IMO 2020 Part 2: Shipowners’ Perspective

Link to article: https://stillwaterassociates.com/imo-2020-part-2-shipowners-perspective/

October 12, 2017

by Ralph Grimmer and Michael Myers

Stillwater is following the progress and impact of the International Maritime Organization’s Global Maximum Sulfur Content of Marine Fuel Rule, or IMO 2020. Our first article, IMO 2020 Part 1: The evolution of the marine sulfur regulation, appeared on the website in September 2017.

The International Maritime Organization (IMO) is moving forward with a marked reduction in the global maximum sulfur content of marine fuel (aka bunker fuel oil) on January 1, 2020. In our September newsletter, Stillwater provided an overview of this “IMO 2020 Rule” along with relevant background. This month, we focus on the shipowners’ perspective on this impending significant change.

An estimated 51,000 commercial ships were registered around the world in 2016. This international fleet can be broken into many specific categories of vessels characterized by size, type of trade, flag nation, area of trade, age, construction, type of propulsion, ownership, and contract operations. Each of these characteristics must necessarily be considered by the owners or operators of the vessels when making decisions on complying with IMO 2020 Rule requirements. At present, it is estimated that less than 1% of the worldwide fleet is operating within the future regulatory limits for sulfur emissions for open ocean areas (i.e. outside of Emission Control Areas).

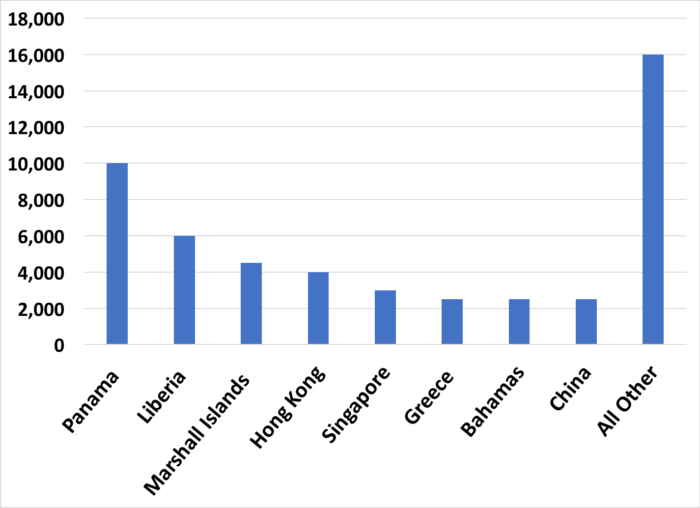

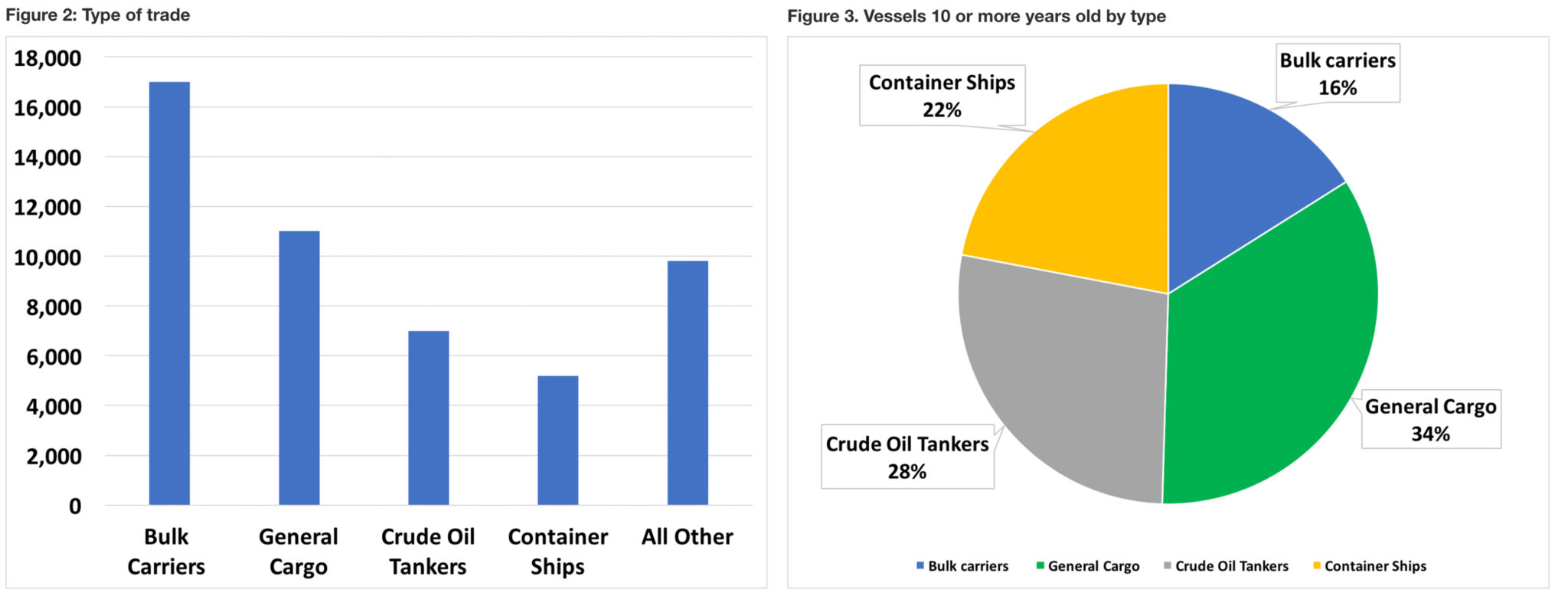

Major categories of global vessels that will be affected by this change can be broken down in many ways. In the figures below, we have broken out the number of global vessels affected by flag country, type of trade, and types of vessels which are at least 10 years old. Note that the top 5 Flag States total 54% of global vessels.

Figure 1. Affected vessels by flag country

Source: Harley Marine

Source: Harley Marine

Marine fuel choice options

Shipowners will be faced with the following basic options for marine fuel sourcing in 2020:

- Use low-sulfur marine fuels – These can be low-sulfur distillates (LSD), a blend of LSD and high-sulfur residual fuel oil (HSFO) or low-sulfur residual fuel oil (LSFO), or some combination. The HSFO component of LSD/HSFO blends will likely be limited to less than 20% to comply with the 0.5 wt. % sulfur content specification.

- Use HSFO – The accepted practice for use of HSFO is with the addition of exhaust gas scrubbing equipment installation. Exceptions to the installation of scrubbers may be an optional “waiver” due to unavailability of compliant low-sulfur marine fuel. IMO currently has no clearly defined mechanism for obtaining this waiver, although work is underway to strengthen this area prior to rule enactment in 2020.

- Use alternative fuels such as liquefied natural gas (LNG) or methanol – The high cost of conversion and current limited availability of infrastructure will make the use of alternative fuels negligible in 2020. LNG facilities also consume roughly double the ship space as bunker fuel oil. LNG usage likely will not be significant prior to 2025. LNG fueling for open ocean vessels will primarily be installed on new-build rather than existing vessels for cost effectiveness. Container ships are a likely candidate for future LNG use.

- Use non-compliant fuels without a waiver – There will likely be a strong economic driver for vessels to use marine fuels that do not comply with the IMO 2020 Rule. This non-compliance may be commonplace where marine operations are not strictly enforced or when market conditions encourage owners to make a choice to operate out of compliance. IMO does not have the authority to enforce its regulations. Such enforcement at present is the sole jurisdiction of Flag States (see figure 1 above). Port States currently have no enforcement authority and are only allowed to notify the appropriate Flag State of non-compliant vessel actions. Flag States typically have small financial penalties for non-compliance and may not be highly motivated to strictly enforce the IMO 2020 Rule.

Factors Impacting Decision-Making

Excluding the options of non-compliance through waiver or disregard (current market conditions combined with lax enforcement expectations favor a significant market share of non-complying vessels in worldwide trade at least initially in 2020), shipowners will be making a choice to use more expensive low-sulfur marine fuel or install exhaust scrubbers and continue to use cheaper HSFO.

There are a number of factors that will be considered when a shipowner contemplates installation of exhaust scrubbing equipment versus use of compliant marine fuel or switching to alternatives fuels for any vessel. These factors include:

- Structural compatibility. Is the vessel’s structural design compatible with the installation? Space to accommodate all the scrubbing equipment may not be available on some vessels.

- Cost of the installation and operation of the equipment. The maritime industry is already financially challenged due to vessel oversupply and very low charter rates. Will the capital cost of scrubber installation (estimated at an average of $4-5 million) be recovered utilizing lower cost high-sulfur bunker fuel oil versus low-sulfur marine fuel? Coming on the heels of IMO’s ballast water management system requirement (nominally $2 million per vessel), the maritime industry faces difficult decisions.

- Age of the vessel. Typical vessel life expectancy is 25 years. In certain trades, the vessels are becoming obsolete in less than 20 years due to innovation and market demands. Can the above capital be recovered before the vessel is scrapped? Given an average capital investment of $4 million and an average fuel consumption of 11,00 MT per year, a price differential of $70/MT would provide a payback in about 5 years. With a 5-year payback, a shipowner would be less likely to make the modifications if the vessel is 10 years or older in certain trades (see figure 3 above).

- Trading routes. Will the vessel be trading almost exclusively within the Emission Control Area (ECA) boundaries requiring more stringent emissions? If nearly 100% of fuel consumption is occurring within these boundaries, the cost of the lower sulfur fuel would have a much more significant impact on operating costs.

- Party responsible for fuel. Is the vessel on contract with a charterer that is responsible to pay for fuel consumption? If so, the owner will be less likely to make the investment in scrubbers than if the owner is responsible to cover the fuel costs. Additionally, a vessel charterer will not be inclined to make the capital investment for scrubbers unless the lease is sufficiently long. Vessel owner/operators will have the strongest case for attractive scrubber installation economics.

- Type of vessel and type of trade. Passenger cruise vessels and publicly owned ferry vessels have a high public profile and will wish to portray their environmental conscientiousness with installation of scrubbers or conversion to alternative fuels. Less-noticed vessels and those trading in third world ports will not have the same incentive to convert.

- Consistency and advance knowledge of routes. Tramp vessels (i.e. vessels without fixed schedules or published ports of call) will likely be less motivated to install on-board scrubbers or switch to alternative fuels such as LNG and methanol than liner vessels (high-capacity, ocean-going ships that transit regular routes on fixed schedules).

- Market conditions. Is the vessel in a highly competitive market which has held down margins long enough to dissuade investment? Much of the world fleet has been in an overcapacity market with reduced or no margins for many years. This situation is forecast to continue for the next several years until the world economy improves.

- Availability of equipment and facilities for modifications. Will the suitable equipment be available, and will there be facilities available to provide quick modifications and return to service? Design to completion of installation can take a year or more to accomplish. If there is a late surge in demand for scrubbing equipment, there will likely be a shortage of equipment and installation facilities available to shipowners wishing to conclude installation in time for 2020.

- Availability of low-sulfure fuel. Will suitable low-sulfur marine fuels be available in the vessel’s trading area? Various fuel grades have been shown to create compatibility issues and engine problems. Marine fuels also require a minimum flash of 60oC as opposed to land diesel’s minimum flash of 52o

- Near-term viability of exhaust gas scrubbers. There is concern by some shipowners that open-loop scrubbers (i.e. effluent water discharged into the open ocean) may not comply with IMO regulations. Closed-loop scrubber systems avoid this problem by discharging the effluent water to an onshore treating facility, but the additional costs, vessel capacity loss, and effluent water receiving systems availability are all factors of concern.

- Longer-term viability of exhaust gas scrubbers. Installation of onboard scrubbers will solve the SOx and NOx issues. However, shipowners who install scrubbing facilities may be at risk of future regulations on carbon emissions and ocean acidification that would undermine the effectiveness of their scrubber investments.

- Economics and availability for alternative fuels. Use of alternative marine fuels such as LNG and methanol will likely be most economically attractive for new-build vessels. Limited locations capable of supplying these fuels will likely result in the initial use of alternative fuel vessels on liner trade routes. Most industry observers do not expect to see a significant shift to alternative fuels until after 2025.

Stillwater’s View

Shipowners are not likely to make significant investments or decisions to modify their vessels in time for the 2020 deadline to allow continued use of HSFO, if that is their primary fuel source. One estimate forecasts that less than 15% of the world fleet will convert to onboard scrubbers by 2020. This procrastination will have impacts on the estimated 2020 fuel grades demand and supply balance.

Global projected marine fuel demand for 2020 is 320 million MT (or over 5 million BPD).

- Consumption within ECA areas estimated at 39 million MT, with 4 million MT being within the North America ECA

- Consumption outside of ECA areas estimated at 250 million MT, with 28 million MT being along the coast of North America

As stack gas scrubbers are installed post-rule implementation, usage of traditional high-sulfur bunkers will likely rebound, but not to current global consumption levels.

Shipowners will predominantly utilize IMO 2020 Rule-compliant marine fuel in the early years of this regulation. As market dynamics, enforcement mechanisms, announced resid-focused refining capital projects, and alternate fuels supply become clearer, shipowners will begin shifting away from compliant low-sulfur marine fuel.

Non-compliance by vessels is likely to be a significant issue. It remains to be seen how successful IMO’s efforts to strengthen enforcement mechanisms will be prior to implementation of the IMO 2020 Rule.

Next month’s Stillwater newsletter will focus on the IMO 2020 Rule from the refiners perspective and highlight some of the key economic considerations driving their decision-making.

We invite your questions and comments on this evolving significant issue.

Tags: IMO 2020, IMO2020Categories: News, Policy, White Papers