Crack Spread: A “Quick-and-Dirty” Indicator of Refining Profitability

Link to article: https://stillwaterassociates.com/crack-spread-a-quick-and-dirty-indicator-of-refining-profitability/

July 28, 2015

by Dave Hirshfeld, MathPro, Inc.

Refining is the key link in the global supply chain extending from the production of crude oil to end-use consumption of refined products. Crude oil as it exists at the wellhead is essentially worthless; a crude oil’s value is in the value of the products made from it.

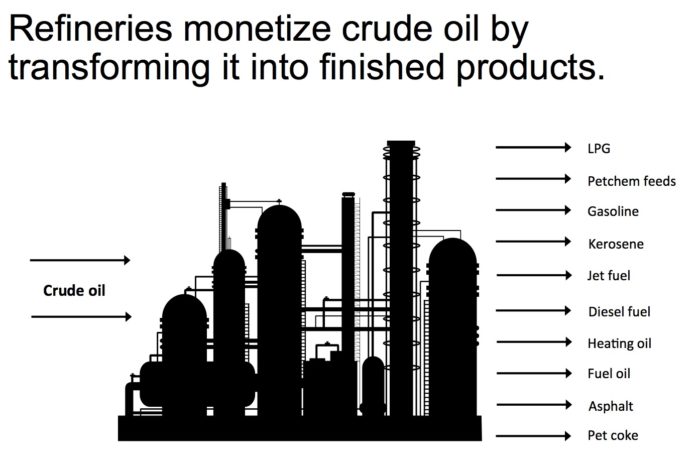

Petroleum products produced from crude oil by refineries, meet more than one third of global energy demand and more than 95% of energy demand in the transportation sector. Refined products range from LPG (propane) – the lightest – through gasoline, jet fuel, and diesel down to asphalt and fuel oil – the heaviest. Light products – primarily the transportation fuels and petrochemical feedstocks – are more valuable than heavy products, such as fuel oil and asphalt. In the U.S., light products (mainly gasoline and diesel fuel) make up more than 75% of the product barrel.

Both sides of the refining business – purchasing crude oil and selling refined products – involve commodity markets, where prices are volatile and beyond the control of any market participant. Prices are subject to sudden, one-off changes, cyclical (e.g., seasonal) variations, and secular, longer-term changes. Except perhaps in the very near term, crude and product prices have proven unpredictable, despite the best efforts of forecasters and market analysts over decades.

Fluctuations in oil prices would not be of great concern to refiners (as opposed to consumers!) if the prices of crude oil and refined products moved in concert. But frequently they don’t. They are subject to different driving forces, stemming from crude oil supply, end-use demand, inventory, and logistics factors – all affected in turn by economic activity, government regulation, and geopolitics.

Crude oil constitutes by far the largest component of any refinery’s direct (variable) operating costs1, and refined product sales are essentially the sole source of revenue. Hence, refining profits are closely linked to the spread, or difference, between the prevailing price of crude oil and the prices of refined products. In the refining industry and in financial markets, this is called the crack spread.2

What Is a Crack Spread?

Crack spread is a “quick-and-dirty” approximation of refining margin.

- Refining margin is the difference between total revenue from refined product sales and total costs of all crude oil and other refinery inputs. Computing refining margin requires detailed proprietary information or estimates of a refinery’s crude slate, product slate, and all the corresponding refinery gate prices.

- Crack spread is defined as the difference between the price of a particular crude oil and a weighted average of the prices of a few refined products, as these prices are registered in commodity markets. Computing a crack spread is simple and requires no proprietary information.

Crack spreads are defined as multi-term ratios, such as A:B:C or A:B:C:D, where

- A, B, C, and D (if present) are integers; and

- A = B + C + (D).

A applies to crude oil barrels, B to gasoline barrels, C to diesel fuel barrels, and D (if present in the crack spread ratio) to distillate fuel or kerosene.

Thus, for example, a 3:2:1 crack spread (the most commonly used crack spread for U.S. refining operations)3 denotes the spread between the cost of buying 3 barrels of crude oil and the revenues from selling 2 barrels of gasoline and 1 barrel of diesel fuel. Similarly, a 6:3:2:1 crack spread denotes the spread between the cost of buying 6 barrels of crude oil and the revenues from selling 3 barrels of gasoline, 2 barrels of diesel fuel, and 1 barrel of fuel oil or kerosene.

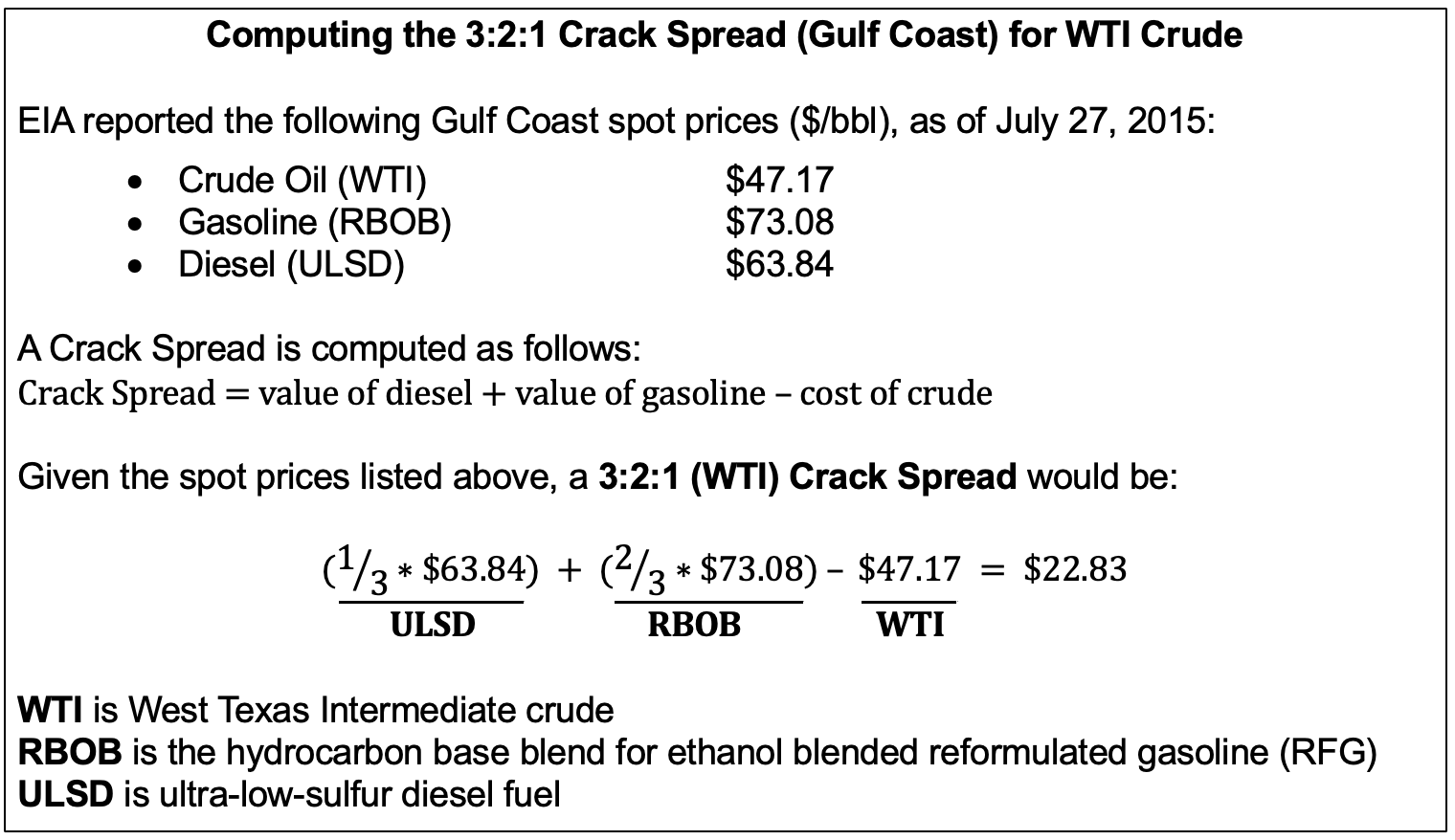

Crack spreads are defined with reference to a particular crude oil (e.g., WTI, Brent, etc.), the specified finished products, and a particular refining center (e.g., U.S. Gulf Coast, NW Europe, Singapore, etc.). The table below shows the computation of a recent U.S. Gulf Coast crack spread, based on published spot prices for the relevant crude and products.

(As this crack spread value suggests, now is a happy time for U.S. refiners. But that’s another subject altogether.)

Current values and historical time series of various crack spreads for different crudes and refining centers (both U.S. and overseas) are available from many sources; some public (e.g., EIA, Scotia Howard Weil, etc.) and some proprietary (e.g., Bloomberg Professional Service, OPIS, Platt’s, etc.).

How Are Crack Spreads Used?

Many refining industry observers and participants – refining industry analysts, government agencies (such as EIA), financial firms, investors – use published crack spreads to (i) estimate the current relative refining values of different crude oils in various regions; (ii) gauge the current refinery profitability in various refining centers, and (iii) track changes in refining sector profitability over time.

Commodity exchanges, such as CME and NYMEX, use crack spreads in a different way. They now offer an array of futures and other derivative contracts based on various crack spreads, by which refiners and other market participants can hedge their exposure to fluctuations in the prices of crude oil and refined products. Trading in these crack spread derivatives has flourished since their introduction because refining is particularly subject to price risk. As we have seen, refiners must deal in markets for both crude oil and refined products. Prices in these markets often do not move in concert, but crack spread contracts enable market participants to hedge their exposure to both markets simultaneously.

_______________________________________________________________________________________________________

1 Other direct operating costs are small in comparison and controllable.

2 The origin of the term crack spread is not clear. It probably was coined by people outside of the refining industry. Outsiders often use “cracking” as a synonym for “refining”, as in, “… a refinery cracks crude oil into gasoline, diesel fuel, and other products…”.

3 The 3:2:1 crack spread approximates the product yield pattern at a typical U.S. conversion refinery: every three barrels of crude processed yields roughly 2 barrels of gasoline and 1 barrel of distillate fuel.

Get expert insights on LCFS, CFP, BC-LCFS, and RFS credit prices.

Stillwater’s Carbon Market Outlooks help fuels producers and investors cut through the noise, navigate carbon market uncertainty, and plan for the future.

Preview a sample reportCategories: Economics, White Papers