Oregon SB 803 Assessment

Link to article: https://stillwaterassociates.com/oregon-sb-803-assessment/

February 23, 2022

Introduction

In late January of 2023, Senate Bill 803 was introduced into the Oregon state Senate.(1) If the bill were to pass, it would require all diesel sold in the Portland metropolitan area (Clackamas, Washington, and Multnomah counties) to meet a carbon intensity of 60 gCO2e/MJ after January 1, 2026, and impose the same requirement in Western Oregon beginning on January 1, 2028, and the entire state of Oregon on January 1, 2030. SB 803 would also limit petroleum diesel to 1% of the diesel sold into these regions as it is implemented which means that 99% would be a combination of two renewable fuels – biodiesel (BD) and/or renewable diesel (RD). This paper describes some of the effects that SB 803 would likely have on fuel cost and supply in Oregon.

Costs of Replacing Ultra-Low Sulfur Diesel (ULSD)

ULSD would have to be replaced by a blend of the two types of biomass-based diesel – biodiesel and renewable diesel. Because BD is chemically different than petroleum-derived diesel, it is limited to a 5% blend (B5) or so in older engines while most newer vehicles have OEM approval for the use of up to 20% BD (B20). The EPA also requires certification of underground storage tanks to be compatible with any diesel blends with greater than 20% BD.(2) Oregon currently requires all diesel sold to contain 5% BD, and the Clean Fuels Program (CFP) has caused BD blending to increase to about 11% of the diesel pool by the second quarter of 2022. By contrast, RD is essentially chemically identical to ULSD, so there is no limitation on its use in diesel vehicles. As such, it would likely make up more than 80% of the diesel supplied if petroleum diesel is banned.

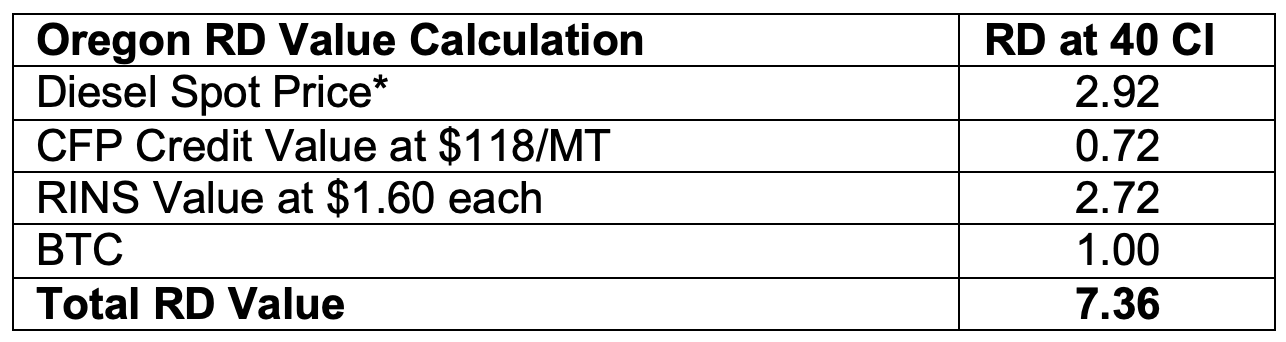

SB 803 has a provision to suspend enforcement of the law if the price of the renewable fuel making up 99% of supply exceeds the price of ULSD. This refers to the price in the market net of all the subsidies provided to renewable fuels and costs added to petroleum fuels to pay for the subsidies. Even though BD and RD are much more expensive to produce than diesel, the price offered to most buyers in the market is usually equal to or less than that of ULSD because of a number of large subsidies provided by state and federal laws. The current price for the most common BD/RD feedstock (soybean oil) is about $0.64 per pound which is $4.86 per gallon. By contrast, the current spot price for ULSD in Portland is $2.92 per gallon(3) so the feedstocks for BD and RD are considerably more expensive than ULSD. To make RD cost competitive, current subsidies from the U.S. Renewable Fuel Standard (RFS) and biomass-based diesel blenders tax credit (BTC) for RD produced from low CI feedstocks such as waste oils total $3.72 per gallon.(4) (BD obtains slightly less in subsidies per gallon because it has less energy per gallon.) The RFS transfers these costs to gasoline and diesel sold in the U.S., while the BTC transfers the cost to U.S. taxpayers.(5) [Note: motorist is using the fuel, but entity impacted is taxpayer.]

RD is mostly supplied into states with incentives such as California with its Low Carbon Fuel Standard (LCFS) and Oregon with its CFP. Under the CFP, RD currently earns credits worth $0.80 per gallon. Petroleum fuel producers who supply Oregon must purchase these credits to be in compliance with the CFP, increasing the costs of producing gasoline and diesel. Adding all these subsidies to the value of ULSD enables calculation of the recent value of RD into Oregon. As shown in Table 1 below, RD is currently worth about 2.6 times the wholesale price of diesel.(6)

Table 1: Current Value of RD in Oregon

*Includes CFP cost to comply.

As long as the subsidies remain in place, both BD and RD can be sold at prices equal to or less than ULSD. However, if one or more of the subsidies is disrupted, this could change. For example, the EPA recently announced bio-mass based diesel (BD and RD) targets for 2023 through 2025 that are significantly lower than expected production capacity due to the expectation that there is not a sufficient supply of feedstocks to fill all of the facilities.(7) If the feedstock supply increases enough to supply this capacity, many more Renewable Identification Numbers (RINS) could be generated than what is needed to meet the Renewable Fuel Standard (RFS) which would cause RINS prices to drop until production is reduced to balance RINS supply with demand. In this case, it could become uneconomical to sell RD and BD at prices below ULSD and the SB 803 provision to suspend the R99 requirement would be triggered.

In Combination with CFP, Banning ULSD Would Shift Costs from Gasoline Consumers to Diesel Consumers

In Oregon, CFP credits add costs to petroleum fuels while reducing the cost of RD and BD, thus making RD and BD competitive with ULSD in Oregon. If, however, petroleum diesel is not available for sale in Oregon as proposed under SB 803, the cost to produce diesel becomes irrelevant and other factors, such as the cost to provide RD, and other technologies as they become available, become the primary driver in determining cost. Consider the situation that sufficient RD/BD supply is obtained to replace diesel. In this case, the number of CFP credits could dramatically exceed the number of deficits generated, causing CFP credit prices to decline due to oversupply in 2026. If CFP credit prices drop 75% from current values, this could reduce the recent value of RD to a producer selling fuel in Oregon by $0.60 per gallon given current CFP CI-reduction targets and recent credit prices.

Although the value of CFP credits to RD and BD producers would likely decline as described above, the cost of producing these fuels would not. Oregon fuel suppliers would have to compete with suppliers in other markets to procure the RD necessary to eliminate petroleum diesel, paying market price even with the above-described reduction in CFP credit value. Since most of the RD is consumed in states with CFP or LCFS programs,(8) other states that do not have this reduction in credit value may have an advantage in attracting the low-CI RD required by SB 803. In this event, the price of the RD/BD blend being sold to displace petroleum diesel would likely increase to cover the reduction in value caused by the decline in CFP credit prices. Consequently, the lower credit prices would reduce the costs of gasoline while the increasing costs of the required RD, by reducing its subsidy under the program. This would have a much greater impact on the cost for businesses to transport goods than for drivers of gasoline vehicles.

This scenario would likely result in the price of the R99 blend being higher than that of ULSD prices in the market since sellers are required to purchase the lower CI RD which has higher value in other markets. In this case, the SB 803 provision to suspend the R99 requirement would be triggered.

Fuel Supply Impacts

Supply impacts of enacting SB 803 are discussed below. These are also likely to impact costs in the fuel value chain.

Supply into the Portland Region in 2026

Should SB 803 pass, it would become mandatory for Portland terminals to sell R99 blends with a CI less than 60 g/mj on January 1, 2026.(9) While Eastern Oregon is supplied by barge up the Columbia River and via pipeline from Utah, and Southern Oregon is supplied by pipeline into Eugene, the counties immediately surrounding the Portland metropolitan area are supplied by truck directly from the six terminals in Portland. As such, beginning January 1, 2026 it would become difficult to supply petroleum diesel to the rural areas immediately surrounding the three Portland counties.

About 44% of Oregon’s population live in the three counties identified for the first phase of the proposed ban in 2024.(10) Another 31% of Oregon’s population live in the counties surrounding these three counties and are supplied by the Portland terminals.(11) As such, roughly 75% of the diesel consumed in-state is supplied by Portland terminals. To enable these adjacent counties to be supplied petroleum diesel would require enabling the Portland terminals to sell it into trucks, which is defined as a wholesale transaction that would be banned under the proposed bill. Given this reality, it would become much more difficult to supply ULSD to the more than 30% of Oregon’s population still technically eligible to use diesel in 2026. In fact, unless there are changes to the legislation, supply of ULSD to the counties outside the Portland tri-county area after January 1, 2026 might have to be from out-of-state terminals.

Between January 2026 and January 2028 when Western Washington sellers must begin to meet the same CFP requirements, there is a chance that under some of the scenarios discussed above that these sellers could be able to price their sales less than those in the greater Portland area because they will not be required to purchase the lowest carbon RD nor the same levels of BD and RD. However, this situation would likely be interpreted as the CFP compliance renewable diesels were being sold at a premium to ULSD, triggering the provision to suspend enforcement.

Emergency Preparedness Program

Post 2030, replacing all ULSD with BD/RD would also likely increase challenges for supply of fuel that is planned for by the Oregon State Petroleum Emergency Preparedness Program.(12) This shift may increase the severity of an unplanned emergency impacting fuel supply. Since ULSD is supplied into all regions of the U.S. and the world, supplies can be diverted from one location very quickly to a location in need of emergency supply. The same would not be true for RD, which is currently produced by a limited number of facilities and is generally only used in California, Oregon, and British Columbia on the West Coast of North America, and in the European Union.(13) In the event of such an emergency, it is likely sufficient quantities of RD would not be readily available so that petroleum diesel might need to be allowed to address the situation on a temporary basis. An appropriate solution to this problem would be a temporary suspension of the SB 803 requirements to enable emergency supply of all types of diesel fuel until the situation returns to normal.

Logistics

The majority (75%) of fuel supplied into the Southern Washington and Portland area is transported through the Olympic (OLY) pipeline from Washington into Portland.(14) This pipeline is full south of Seattle, and an additional 25% of fuel supply is delivered by ships and barges into the Southern Washington and Portland area terminals. BD and RD are not transported on the Olympic pipeline, so all BD blended in the Portland area is brought in by rail or barge.(15) Based on the above supply analysis, SB 803 would likely change demand into Portland from being about 90% ULSD to less than 50% ULSD. Unless the Olympic pipeline begins to allow RD on the pipeline along with ULSD, larger volumes of waterborne shipments would be required.(16) Even if Oly allows batches of both RD and ULSD, these would need to be kept segregated in the pipeline and at Portland terminals to allow ULSD to be supplied into Eugene through the Kinder-Morgan pipeline. This would increase the need for storage tanks required to ratably supply the same volumes. The projected increase in BD which must be segregated from RD and ULSD would also increase the need for storage tanks. The Portland terminals would therefore need to expand in order to handle and segregate the three different types of diesel fuels being distributed. If these expansions are not permitted, supply could become much more difficult and less reliable. This kind of supply impact could lead to shortages or outages.

Lastly, the federal government requires specific labelling for any retail sales of diesel with more than 5% RD, so the transition away from petroleum diesel will require labels at every point of sale in the state. Since Oregon already requires the diesel pool to be at least B5, the labels for BD should already be in place.

(1) https://olis.oregonlegislature.gov/liz/2023R1/Downloads/MeasureDocument/SB0803/Introduced

(2) https://www.epa.gov/ust/emerging-fuels-and-underground-storage-tanks-usts#tab-2

(3) Source: OPIS Reporting on 2-2-23

(4) Ibid.

(5) The BTC is a tax credit for an entity which blends the BD or RD into petroleum diesel which reduces U.S. Federal Tax Revenue. This blend results in a $1 per gallon credit toward its federal tax liability. This required blending is why R99 (99% RD) is sold. Also, there are retail labelling requirements for any diesel blend with more than 5% BD and/or 5% RD. https://www.eia.gov/todayinenergy/detail.php?id=42616

(6) OPIS Reporting on 2-2-23 and Stillwater Analysis.

(8) Stillwater analysis of CARB, DEQ, and other public information.

(9) In December of 2022, the Portland City Council passed a resolution banning the sale of petroleum diesel that also requires the CI of BD and RD used to be less than 40 g/mj. This more stringent standard will complicate supply because the waste oil feedstocks used produce low CI renewable fuels are projected to be in short supply. Diesel demand in the city of Portland is about one third of that of the three-county area.

(10) https://www.oregon-demographics.com/counties_by_population

(11) Ibid.

(12) https://www.oregon.gov/energy/safety-resiliency/Pages/Petroleum.aspx

(13) Stillwater analysis of publicly available information.

(14) Ibid.

(15) Ibid.

(16) Note that BD will probably not be allowed on the Olympic pipeline due to potential contamination of jet fuel also shipped on the line. See https://www.api.org/~/media/files/oil-and-natural-gas/pipeline/aopl_api_ethanol_transportation.pdf.