California Gasoline Prices – Part 2

Link to article: https://stillwaterassociates.com/california-gasoline-prices-part-2/

June 26, 2019

By Dave Hackett

Last month, I wrote about spot California gasoline prices and promised to write about California retail gasoline prices this month. As explained by my Petroleum Market Advisory Committee (PMAC) colleague, Professor Severin Borenstein, the retail gasoline prices in this state are higher than the U.S. average, even after deducting California’s high taxes and fees.

Just this week, the Energy Information Administration (EIA) reported that the average Regular retail gasoline price in the U.S. was $2.65 per gallon while California’s average price was $3.61 ($0.96 per gallon higher than the national average). California’s taxes and fees run about $0.50 per gallon higher than the U.S. average, so the additional price gap is about $0.46 per gallon more than is easily explained. That $0.46 per gallon accumulates along the supply chain, created by higher product and distribution costs, and wholesale and retail margins.

This “mystery surcharge” came up with PMAC because prices rose dramatically in 2015 due to refinery issues. However, after the refinery problems were fixed and spot prices dropped, the retail prices stayed relatively high. The question is, why isn’t competition doing its usual job of bringing retail gasoline prices down to “normal” levels? The answer to that question has several components:

First, the market structure has changed. In the past, integrated oil company operations focused on upstream profits and defending gasoline market share. ARCO, the low-price leader, used to battle for market share in order to maximize the monetization of its abundant Alaska North Slope crude supply. They owned all their own stations and had control over the price-sensitive segment of the consumer market. BP bought ARCO some years ago but sold the gas stations off to franchisees. BP was not driven by retail market share like ARCO had been. Then Tesoro bought BP’s Southern California business, including all their ARCO stations in SoCal. Tesoro transitioned the ARCO image to higher quality through the adoption of “Top Tier” gasoline.

Back in the day, when spot prices shot up, gas station operators at the price-sensitive end of the market moved their retail prices up because their wholesale purchase price, tied to spot, went up. ARCO, however, didn’t raise prices. Often, the price-sensitive operators temporarily shut their stations down because their costs were now too high. When those “low pricers” temporarily shut down, their customers shifted to ARCO, increasing ARCO’s market share. That doesn’t happen anymore. When the spot price goes up, ARCO’s goes up with it.

The other California refiners, in many cases, aren’t marketers anymore. Companies like Mobil, Union, Shell, and BP sold all or many of their stations to smaller companies or to their franchisees. The companies, or their successors, continue to supply the gasoline and license the brand to the new owners.

These refiners used to employ sales representatives whose job it was to ensure compliance with the brand image. They also were trained to counsel franchisees on street-pricing strategies in order to maximize sales. This often left the franchisees with thin per-gallon margins.

Today, these refiners don’t have company-owned stations and their sales reps aren’t pushing on the franchisees to get street prices down.

Because many of the stations are now owned by franchisees, these owners have learned that higher margins are important to their standard of living.

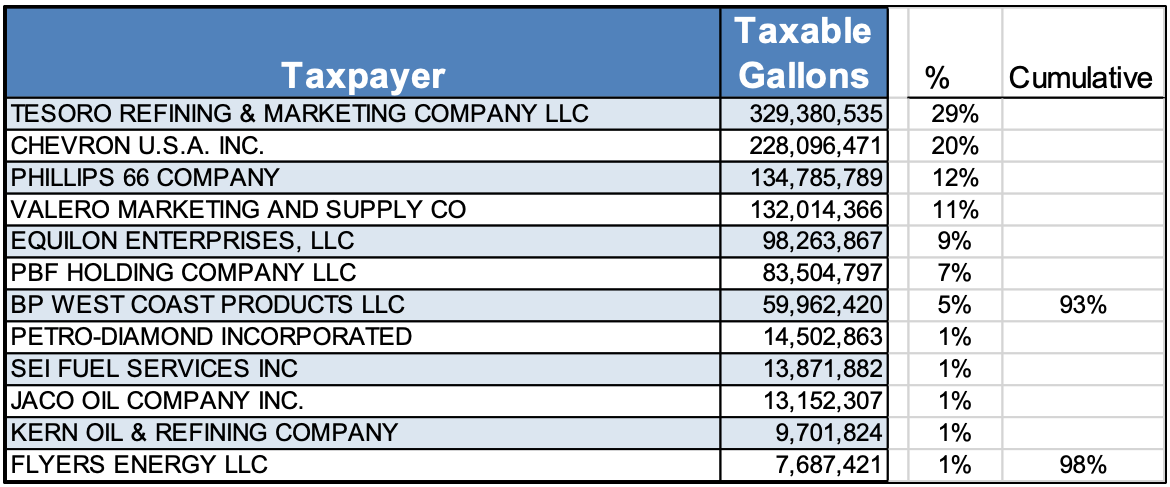

Second, the market is concentrated in a non-obvious way. Two competitors, Chevron and Marathon (formerly Andeavor/Tesoro) supply about 49% of the market, according to statistics from California’s Department of Tax and Fee Administration (DTFA). The concentration is non-obvious because Tesoro accumulated a large number of stations from other companies and retained those stations’ brands. Tesoro’s products are marketed under brands like ARCO, Exxon, Mobil, Shell, Thrifty, and USA.

DTFA’s “Taxable Gallons Report” shows which firms are paying excise taxes to the state when gasoline is loaded onto a truck for delivery to the gas station. That data is displayed in Table 1 below.

Table 1. Motor Vehicle Fuel Distributions Report (February 2019)

Much of the volume that Tesoro and Chevron produce are priced delivered to the gas station, which means they have close control over what the franchisee pays.

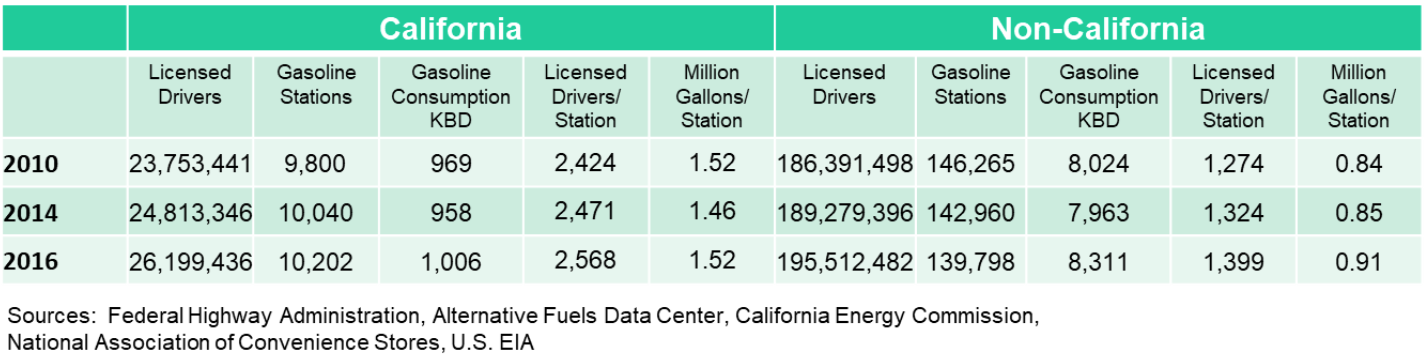

Third, there are barriers to new entrants, as evidenced by the number of gas stations. Stillwater analyzed the market and found that there are nearly twice as many drivers per gas station in California compared to the national average. Table 2 displays this gas station data.

Table 2. Driver and Station Data – California vs non-California

So, why aren’t more stations being built? “New-to-industry” stations seem to only be coming online in the growing zones outside of major metropolitan areas, probably because land prices and lengthy permitting processes make new urban gas stations unattractive to investors.

In some cases, government regulations restrict gasoline sales. For example, at a big-box store near Stillwater’s headquarters, the gas station frequently has to shut down before the end of the month because it exceeds the monthly gallonage permit from the local government. Its customers have to switch to a higher-priced station or wait until the first of the month to fill up.

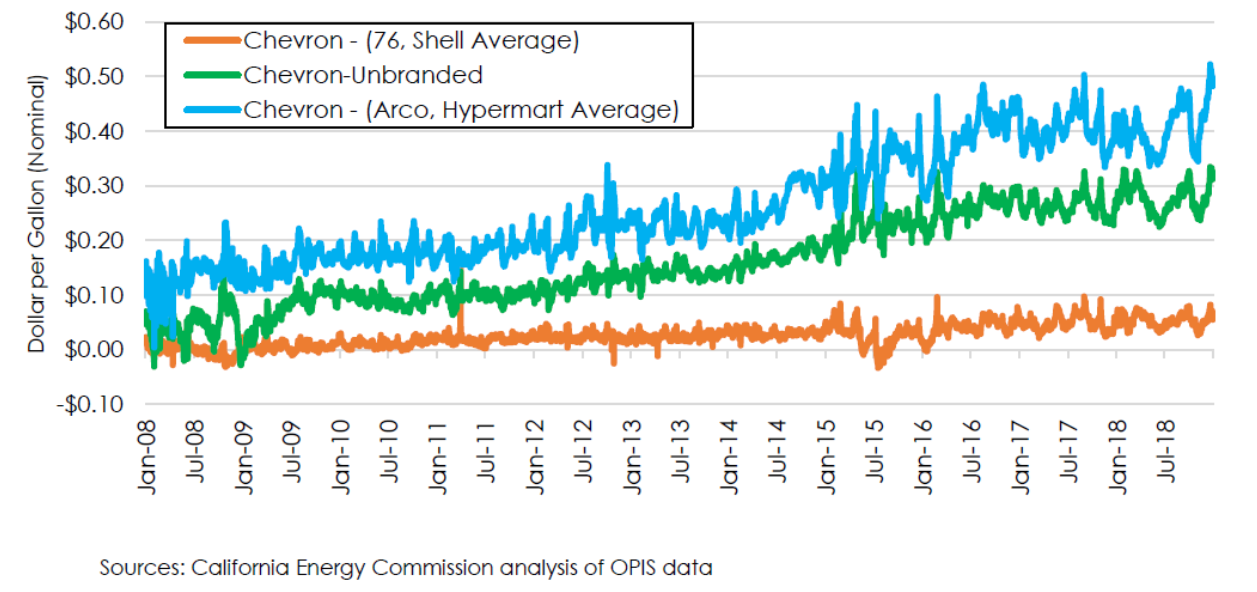

Fourth, over time, the major brands have increased their retail prices, relative to the independents. The California Energy Commission (CEC) performed an analysis around this phenomenon and updated that analysis in May. We include the CEC’s graph as Figure 1 below.

Figure 1. Price Differences between California Gasoline Retail Brands

In their memo to the Governor,[1] the CEC wrote: “So while higher-priced retail brands such as Chevron, Shell, and 76 are expanding their price premium relative to other gasoline retailers, their combined market share has hardly changed indicating a low sensitivity to price changes by their customers.”

This issue has been a bit of a head-scratcher for us. We’ve concluded that the big-box stores (Hypermarts on the CEC graph) are running at full capacity and the folks who go to Chevron, Shell, and 76 don’t want to wait in line.

Thus, when asked why prices are so high, my response has been “There aren’t enough Costcos.”

[1] California Energy Commission. Gasoline Prices in California. May 15, 2019.

Tags: gas pricesCategories: Economics, Wisdom from the Downstream Wizard